Fund Investing

Written By: Milja Mieskolainen

If we start talking about fund investing, the first thoughts include at least the idea of high costs, the blurring of the final destination of the money, and perhaps a doubt about reliability. The world of funds, like the real world, is complex, so a researcher may quickly become confused. In this post, we discuss fund investing at a general level, and look at the most common fund types and their characteristics. ETFs, or exchange-traded index funds, are excluded from this post: You can read more about them here.

Let's start with the definition of an investment fund: At a general level, it refers to a fund maintained by a management company, which may consist of, for example, shares or other securities, in which the assets of several individuals are pooled. Fund investing can be seen as an intermediate form of equity investing and account saving, making it an easy way to start investing. The investor owns a share of the fund corresponding to his/her investment, while in an equity investment, the investor buys a certain number of shares for a certain amount of money, thus owning “whole” shares. There are tens of thousands of different investment funds worldwide, so at least there is no shortage of choice.

Fund categories

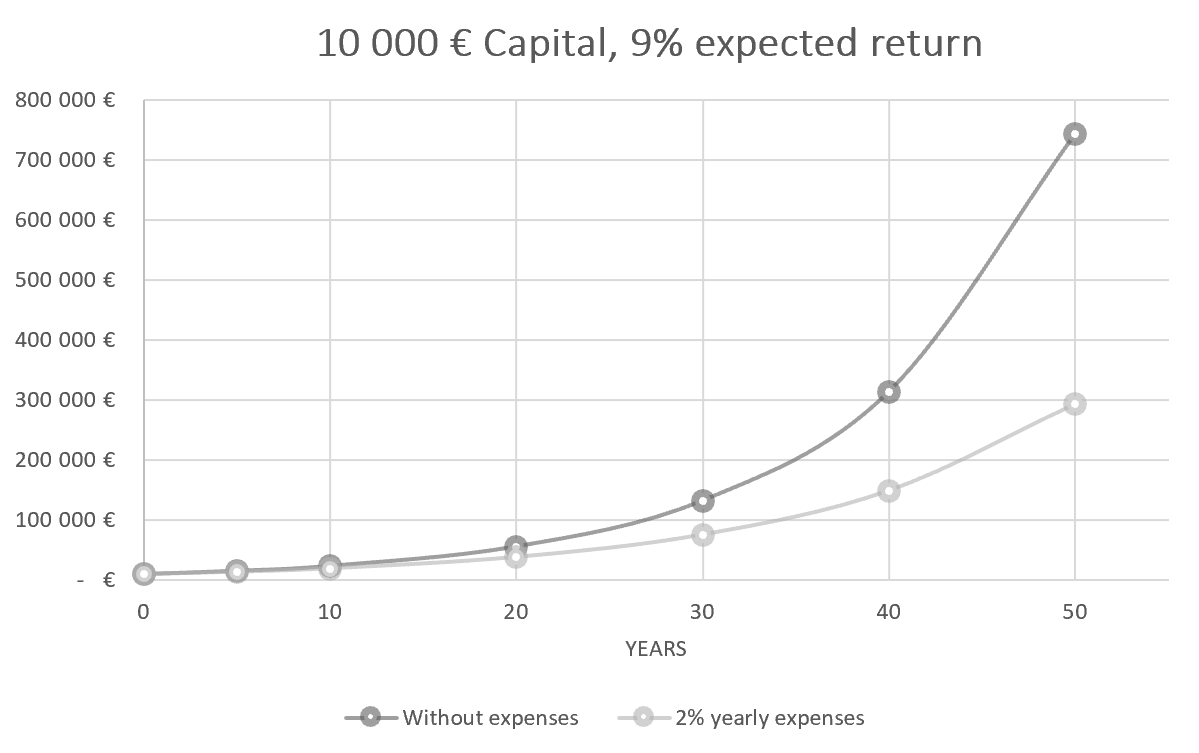

Typically, funds are divided into two or three groups. In active funds, the portfolio manager takes care of investment decisions. It is also possible that the portfolio manager will use the management company’s quantitative investment strategy as a basis for his/her decisions. In these funds, management costs are usually quite high (1.0-2.5%) and may also include performance-related fees. While management fees, such as 2%, may sound small at first, their impact, especially on long-term investment, increases significantly, as can be seen from the graph above. In addition to management and performance-related expenses, the fund may also charge the investor subscription and redemption fees. It must be remembered that the costs of the funds are not identical and can differ significantly.

The benefit of an active fund is usually considered to be the professionalism of the portfolio manager. Some investors are willing to pay more for a professional view that they hope will lead to a better returns. Another reason for accepting high costs may be that the investor feels that he or she does not know the scope of the mutual fund's objects: For example, the oil market may seem distant to someone, so he/she chooses a fund to invest in.

Passive funds follow their benchmark / target index without the active decision-making of the portfolio manager. These funds cannot therefore achieve higher returns than the market. In general, it can be said that passive funds are better for the investor because of the lower costs (0-0.6%): They are easy to manage and there are many different options available.

There is room for another, not so pleasant, fund type. About a couple of per cent of Finnish fund investments are in index funds (Cremers, Ferreira, Matos and Starks, 2013). According to the same study, about half of Finnish fund investments are in actively managed funds. Where does the remaining about 45% go? In free translation, the study referred to above calls these funds “cabinet index funds”: These are sold under active management, but in reality they mimic the index. These funds charge all the same costs as actively managed, but make investments entirely according to the market index.

Fund types

Below is a list of the most common fund types. We do not go into the contents of the funds in more detail in this post, but you can read them here, for example, if you wish. In addition to the ones below, the funds can also be divided within an asset class, for example, an equity fund can only target Finnish or European shares.

• Equity funds

• Fixed income funds

• Combined funds

• Index funds

• ETF, ie index unit fund

• Funds of funds

• Leverage funds

• Hedge fund

• Forest funds

• Real estate and housing funds

Income or growth fund?

Different shares may be available in the funds. In a income fund, the investor receives a regular return on the profit share directly in his or her bank account. These may be suitable for an investor who wants a steady cash flow from their investments. There is no redemption fee for income shares, but capital gains tax is paid on the income, which is why these are quite rare among small investors.

Growth funds thus avoid taxing income: they reinvest dividends, interest income and capital gains, thus taking advantage of the interest on interest phenomenon. The payment of taxes to the owner of the growth unit comes to the fore only when he decides to redeem his investment.